IoT時代、ディスプレイを中心とするスマートインタフェース

新しいIoT時代が到来するという2015年Googleの発言から、今後迎えるスマートインタフェース時代をテーマに中国の大型ディスプレイメーカーであるBOEの発表を皮切りに、第13回「China International Display Conference」が幕を開けた。

Randy Chen(BOE、営業マーケティング総括)氏は、最初の発表に合わせてIT市場全体の動向についてまとめながら、BOEの戦略を説明した。2050年には約10兆米ドルに達すると見らているIoT産業の中心には、5G通信と電子機器をディスプレイで結びつけるスマートインタフェースが、大きい役割を果たすようになり、BOEの生存戦略として8Kとフレキシブルディスプレイを強調した。その実現に向け、8K産業連盟の構築に取り組んでおり、中国四川省成都にあるG6フレキシブルラインを始めとするフレキシブルディスプレイを製造するために、投資を継続していると発表した。今年の下半期に稼働を開始した成都のB7ラインで製造されるOLEDパネルは、中国広東省深川にあるスマートフォンメーカーに納品され、来年初めには市場で見ることができると期待される。

続いて、PMOLEDを始め、最初にOLED製造を開始したVisionoxのXiuqi Huang(GVO、Vice President)は、スマートフォンのトレンド変化について述べながら、今後フレキシブルパネルをを採用したFordableやRollable形状のモバイル機器が登場すると語った。フレキシブルパネルの様々な形状変更によって、デザインのみならず、関連装置と材料にも技術開発が必要で、Visionoxも積極的に技術開発を進めていることを明らかにした。

Samsung DisplayとともにQD-LCDを製造している代表的な企業CSOTは、QLEDとOLED TVの発展可能性について述べ、後発者として技術開発と投資に拍車をかけていることを伝えた。特に、相対的に高い材料使用率と価格競争力という利点を持っている大面積インクジェットプリント技術の開発に取り組みながら、ベゼルを最小限に抑えるスマートフォン用パネルの開発目標についても共有した。

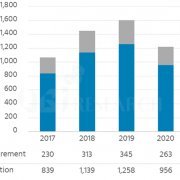

中国の代表的なパネル企業の発表に続き、グローバルOLEDリサーチ企業UBI Researchのイ・チュンフン代表は、既に中小型パネル市場とプレミアムTVパネル市場をリードしているOLED市場の規模を予測し、なぜOLEDが次世代ディスプレイとして急成長できたかについて語った。UBI ResearchはOLED専門リサーチ企業で、長年にわたり蓄積したデータとリサーチ経験を活かし、今後OLEDの成長の方向性を示した。

現在、ディスプレイ産業では、Apple、Samsung、Huaweiなど、世界の主要スマートフォンメーカーが、既に全てのフラッグシップモデルにOLEDを採用する計画を立てており、LG ElectronicsとSonyなどのTVメーカーもOLED TVがプレミアム市場で成功すると確信している。それが今後OLEDが持っている利点を極大化した様々な形状のパネルとアプリケーションの発展が期待される理由である。